Q&A regarding management strategies for achieving long-term growth

This Q&A has been prepared to provide our investors with a deeper understanding of the background behind our sustained growth over many years and to outline our medium- to long-term management direction for the future. It presents our perspectives on a wide range of topics—including the significance of our business diversification, the future outlook for each business domain, our approach to global expansion and M&A, and our stance on corporate governance and shareholder engagement.

Through this Q&A, we aim to convey a comprehensive view of our management strategy and reaffirm our continued commitment to enhancing corporate value in a sustainable and long-term manner.

Q1. Reason for the Disclosure of Rohto Pharmaceutical’s Medium- to Long-Term Growth Strategy and Outlook (May 2025)

We have consistently provided timely disclosures and explanations of short-term information, including quarterly financial results. However, with respect to medium- to long-term growth strategy, we have deliberately avoided a goal-driven planning approach that rigidly targets specific outcomes. Instead, we have adopted a strategy of updating our plans annually to enable agile and dynamic decision-making. As our business domains have expanded and our diverse operations have become increasingly interconnected and complex, we recognize that it has become more challenging for stakeholders to gain a comprehensive understanding of the overall structure of our business.

While our Integrated Report (Well-Being Report) has been prepared with the intention of presenting this overall picture as concretely as possible, we decided to disclose our medium- to long-term growth - together with the underlying strategic framework - in order to enhance stakeholders’ understanding of our management direction and long-term vision. This outlook will be reviewed and updated on an annual basis. It should be noted that the figures and projections presented herein do not represent a fixed view of what we will necessarily achieve in five years. Rather, they are based on the premise that we will continue to make flexible and timely management decisions aimed at further enhancing our corporate value.

Our integrated report (Well-Being Report) has been edited to convey the overall picture as specifically as possible, but we have decided to create and publish the mid- to long-term outlook, which forms the core of the report, and the fundamental business strategy that underpins it, in order to help all stakeholders understand it.

This content will be reviewed annually and updated accordingly. This does not mean that it will necessarily be like this in five years, but rather that we will continue to make decisions as needed to further increase our corporate value.

Q2. Why does Rohto Pursue Diversification Across Multiple Business Domains?

A strategy that focuses corporate resources on selected strong business areas can be effective when markets are stable, growth is predictable, and competitive dynamics remain relatively unchanged. However, in today’s VUCA environment, relying solely on a single business or market causes significant structural vulnerability.

Our founding business, OTC medicine in Japan, has long operated in a gradually contracting market environment. Although we have benefited from the exceptional growth of the eye drops market within this sector, driven by increasing demand over the years, future stagnation will be inevitable due to Japan’s declining population. As a result, even our core business faces limitations in terms of major expansion.

For many years, we have been committed to fostering a corporate culture and developing human resources capable of venturing beyond specialized fields to explore new areas of demand adjacent to our core businesses. This approach has enabled us to build a strong foundation of non-financial assets—particularly organizational adaptability and resilience—that provide a competitive advantage in responding effectively to changing circumstances.

Furthermore, the Japanese OTC pharmaceuticals market, which is our original business, has been in a state of gradual long-term contraction. Within this environment, the eye drops market has seen exceptional growth in demand, which has benefited us. However, going forward, stagnation due to the declining population is inevitable, and it is thought that significant expansion of Core businesses will be difficult.

We have long been working to develop human resources and foster a corporate culture that allows us to explore new demand surrounding our Core businesses, rather than being confined to our own specialized fields. This gives us an advantageous non-financial asset in terms of our ability to adapt to changing circumstances.

*Please also refer to Takashi Nawa's "Super Evolutionary Management," Nikkei BP, 2024, pp. 135-154.

*Please also refer to Akira Iriyama's "Global Standard Management Theory," Diamond Inc., 2019, pp. 452-453.

*Please also refer to International Business Journal, September 2025, Vol. 58, No. 688, P16-41

Q3. Outlook for the Cosmetics Business, Which Has Achieved Strong Growth to Date

Our cosmetics business has achieved significant success through the creation of groundbreaking products inspired by pharmaceutical concepts, combined with the expansion of a new sales channel—the drugstore. Today, drugstores have become the primary retail channel for cosmetics sales, where we have secured the No.1 position in terms of sales volume. This success can be attributed to factors such as high customer satisfaction and strong evaluations of cost performance, as well as word-of-mouth recommendations and social media advocacy. Unlike conventional cosmetics brands that emphasize glamorous brand imagery as their core value, our strength lies in the trust and positive experiences of real users. Going forward, the key to sustained growth will be the continued development of science-based, high-quality products that incorporate cutting-edge ingredients and formulation technologies.

In recent years, aesthetic dermatology has become more accessible, and consumers increasingly expect professional-grade results. As such, ingredient development based on medical research and expertise derived from regenerative medicine are becoming essential to innovation in this field. While this area remains in an early stage of development, the overall cosmetics market remains vast, and we believe there are ample opportunities for further business expansion.

We have now achieved the number one position in terms of sales volume in drugstores, which have become the main channel for cosmetics sales. While existing cosmetics have a flashy brand image as their core value, our cosmetics are sold largely because many consumers are satisfied with them after actually using them, evaluate their cost performance, and receive recommendations from acquaintances and on social media. Going forward, our biggest priority will be to develop excellent science-based products that incorporate the latest ingredients and formulation technologies.

Furthermore, in recent years, cosmetic dermatology has become more commonplace, and people are now expecting more professional and reliable results, making it essential to develop ingredients inspired by medical science and to have know-how from Regenerative medicine field is still immature, and the overall cosmetics market is very large, so we believe there will be great opportunities for our business expansion in the future.

Q4. How Is the Competitive Landscape in the Cosmetics Business Expected to Evolve?

Competition with existing major players remains intense, with market share battles taking place on a daily basis. In recent years, however, the industry structure has been undergoing significant transformation. The rapid growth of fabless emerging brands driven primarily by marketing, the increasing popularity of private brands developed by large-scale drugstore chains, and the rise of ODM manufacturers supporting these trends are reshaping the competitive landscape. We anticipate that these developments will present major challenges going forward.

In addition, cosmetics from Korea and other parts of Asia are gaining popularity, particularly among younger consumers such as Generation Z, further intensifying competition. To address these changes, our core strategy lies in strengthening our scientific expertise, which is one of our fundamental strengths. At the same time, we aim to capture emerging marketing trends quickly through our Asian subsidiaries and continue to launch new brands targeted at younger generations.

Notably, “Hadalabo” and “Melano CC” were both launched as new brands and have grown rapidly in the market. We consider the ability to establish and scale up new brands swiftly to be one of our key competitive advantages.

Furthermore, Korean and Asian cosmetics are becoming popular among young people known as Generation Z, further intensifying competition. To compete in this market, we will fundamentally focus on mastering science, which is our strength, but at the same time, we will continue to quickly adopt marketing trends from our Asian subsidiaries and launch new brands through marketing targeted at younger generations. Hada Labo and MELANO CC were also launched as new brands, and we believe that the rapid launch of new brands is one of our strengths.

Q5. Will Rohto Continue to Invest in Their Own Manufacturing Facilities?

We believe that in order to create truly differentiated products, it is essential to develop manufacturing technologies within our own facilities. At the same time, we will continue to maintain strong partnerships with leading ODM manufacturers, particularly in areas where they possess technological strengths or speed that complement our own capabilities.

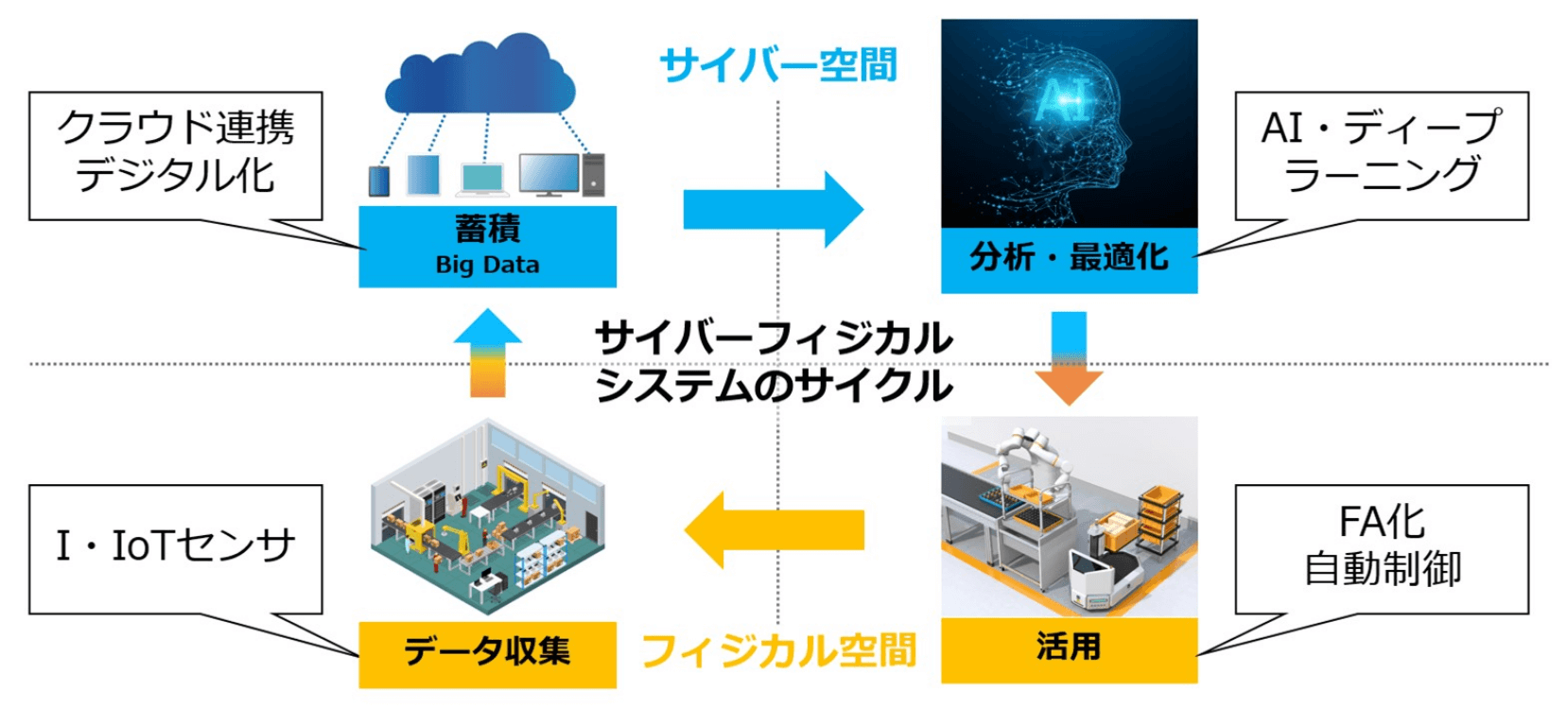

Our production technology divisions, which underpin our manufacturing excellence, will play an increasingly important role as we expand globally. We are advancing the development of digitally integrated smart factories (CPS: Cyber-Physical Systems) and plan to establish next-generation facilities both in Japan and overseas, incorporating technologies such as AI and humanoid robotics. In Japan, the manufacturing sector faces a nationwide shortage of workers. While we are promoting automation and unmanned operations, securing and developing employees who can operate and manage these advanced systems is also a key priority. For this reason, our factories are not treated as separate organizations but as integral divisions of our core operations, with initiatives to professionalize and enhance the expertise of regular employees.

From a global perspective, we have pursued a local production for local consumption strategy by establishing manufacturing and supply chain networks as close to local markets as possible. In light of the recent rise in trade barriers between regions, we believe this approach has proven to be both timely and effective. Looking ahead, we plan to continue making proactive investments in manufacturing facilities, particularly to meet growing demand in emerging markets.

From a global perspective, we have been developing factories and building supply chains with the aim of "local production for local consumption," which means producing as close to the market as possible, and in recent years, with trade barriers between regions increasing, we believe this strategy is the right one now more than ever. We plan to continue to actively invest in factories in emerging markets.

Q6. What Is the Future Outlook for the Department Store Cosmetics Business?

Although department stores—once a dominant retail format across Japan’s major cities—have faced challenging conditions, we have concentrated our presence in top-tier department stores in major metropolitan areas such as Tokyo and Osaka. These stores continue to perform well and attract strong inbound demand from overseas visitors. Our “Episteme” brand has now been firmly established over the past 15 years, holding a solid presence among leading domestic and global luxury brands. In particular, the “Stem Science series”, which incorporates regenerative medicine technology, has gained strong popularity. This premium category has strengthened our brand credibility through features in magazines and endorsements from beauty experts and influencers. The resulting online exposure has further enhanced our corporate value in the eyes of consumers.

Our skin consultants, who serve customers at department store counters, are employed as regular staff, and their skills in personalized consultation have contributed not only to the in-store experience but also to customer service excellence in drugstores, e-commerce, and call centers. Going forward, our department store brands—which represent the pinnacle of our technological expertise—will serve as flagship brands to be expanded globally alongside other leading luxury brands.

This department store brand, which brings together the best of technology, will expand globally as a flagship brand that can rival overseas luxury brands.

Q7. Can We Continue to Succeed in the Highly Competitive Hair Care Market?

The hair care market is fiercely competitive, with numerous powerful players, but we aim to provide unique values through science-based product innovation. Our medicated shampoos for scalp conditions such as dermatitis and dandruff have been steady-selling products in Japan for nearly two decades. Overseas, our “Selsun” and “50 Megumi” brands enjoy strong popularity, particularly across Asia. In addition, our “DEOU” and “DEOCO” brands, focused on odor care, have established loyal user bases.

“GYUTTO”, launched last year, became a hit by applying university-led research into hair structure to deliver benefits from a completely new perspective. Our minoxidil formulations are steadily growing in the e-commerce channel, and we see significant business opportunities—both domestically and internationally—in developing hair-growth products that activate follicle stem cells and color treatments that offer both high efficacy and scalp gentleness. We believe that hair care, even more than skin care, presents vast potential for future expansion.

Q8. What Is the Outlook for the Eye Care Business?

The domestic OTC eye drops market has continued to grow moderately, even as the overall OTC sector has stagnated. However, we expect future growth to come primarily from higher-value, multifunctional products rather than increased volume. Overseas, the use of eye drops is not yet as widespread as in Japan, suggesting significant growth potential. As we have been steadily developing and registering products tailored to each country’s regulatory environment, we anticipate steady expansion in the global market. In the medical field, we are developing innovative products not currently available in the market, with the first launches expected within the next two to three years—creating entirely new business opportunities. Additionally, “myopia prevention” is drawing attention as an emerging healthcare need, with new pharmaceuticals and supplements expected to appear in this category. We are actively pursuing development in this area, viewing it as a promising long-term growth domain. Beyond pharmaceuticals, we are also engaged in the development of surgical instruments, digital devices, and cell-based therapies, aiming to establish ourselves as a comprehensive provider of eye care solutions.

In the medical field, we are currently developing new products not yet available on the market, and the first products are expected to be launched within the next two to three years, making these a plus-on business. Furthermore, the prevention of myopia has been gaining attention in recent years, and with corresponding pharmaceuticals and supplements expected to appear in the future, it is expected to become a large market in the medium to long term, and we are also promoting development in this field. Additionally, we are working on the development of surgical instruments and materials, digital devices, and cell therapy drugs, and will cover a wide range of fields as a comprehensive eye care provider.

Q9. What Is the Future Outlook for the Oral Medicine Business?

Our gastrointestinal medicines, such as “Shiron” and “Pansiron”, have been cornerstone products since our founding and have long supported our growth as top-selling brands in the Japanese market. Although intensified competition has placed these brands within the third-tier group in recent years, “Panshiron Cure”—targeting acid reflux—has been well received, showing signs of brand revitalization.

Our “Wakansen”, herbal medicine series, has been struggling, and we plan to maintain its current level for the time being. In contrast, our “Rohto V5” eye care supplement series has performed strongly, generating over 5 billion yen in annual sales—mainly through our own e-commerce channels supported by a solid base of loyal subscribers. While our own e-commerce business started later than competitors, our focus on high-functionality products rather than low-value, generic supplements has proven successful. We will continue to broaden our product lineup around these loyal users to drive further growth.

On the other hand, Wakansen, a traditional Chinese medicine, is struggling, and we plan to maintain the status quo for the time being. Instead, ROHTO V5 series of eye care supplements has been doing well in recent years. While it is also sold in stores, mail order sales exceed 5 billion yen annually, and with the support of loyal regular customers, we expect further growth. Our mail order business has been slower than other companies, but we have been fortunate in that we have chosen not to enter the market for simple ingredient supplements with low added value, but have instead focused on highly functional products. Going forward, we plan to expand the range of our product proposals, with these loyal users at the core.

Q10. What Is the Strategy Behind the Acquisition of Eu Yan Sang International (EYS), and What Returns Are Expected?

Our strategy is to leverage EYS’s numerous strengths—including its 146-year-old brand heritage, its expertise in high-quality traditional Chinese medicine, herbs, and food products, its base of 650,000 active customers in Hong Kong, Singapore, and Malaysia, and its integrated retail and clinic network—to establish a leading position in the shift from chemical-based vitamin and mineral care to Natural Health & Wellness.

Although current results are below initial expectations, this is mainly due to economic slowdowns in Hong Kong and Singapore—EYS’s core markets—and the lower-than-expected demands of the high-end gift segment. In response, we are pursuing cost reductions through higher in-house production and developing new, more affordable product lines to attract new customers, supported by strengthened marketing leveraging the expertise of the Mentholatum Company.

Through this acquisition, our Asian sales have surpassed 100 billion yen. By combining the strengths of the “Mentholatum” brand in skin care with EYS’s capabilities in oral and food-based wellness, we aim to become a unique, integrated self-care provider across Asia.

While current business performance is below initial targets, this is primarily due to the general economic downturn in our main markets of Hong Kong and Singapore, and in particular the greater-than-expected contraction of the luxury gift market. In response, we plan to reduce costs by promoting in-house production, develop products that can attract new customers at more reasonable prices, and strengthen marketing activities that utilize the knowledge of The Mentholatum Company, Inc..

With this acquisition, sales in Asia will exceed 100 billion yen, and by combining the mutual resources of the Mentholatum brand, which is strong in skin care, and EYS, which is strong in oral medication and food, we aim to become a one-of-a-kind self-care provider.

Q11. What About Other OTC Fields? Will We Enter New Market Segments Where We Are Not Yet Present?

Our “Mentholatum” brand of topical treatments continues to perform strongly, with “EXIV”—our athlete’s foot medication—now established as a market leader despite being a later entrant. Our “DoTest” line of pregnancy and ovulation test kits, which we were the first to introduce as OTC products in Japan, also maintains its position as a top brand. Should new testing categories become available for OTC sale, we expect to leverage the “DoTest” brand for effective market entry.

Conversely, we have not entered larger OTC segments such as energy drinks, vitamins, cold remedies, pain relievers, or patches. Given the limited growth prospects and high brand dominance of existing players in these markets, as well as the challenges of clear product differentiation, we currently see little strategic merit in entering these categories.

Q12. What Are Our Expectations for Switch OTC Products?

In Japan, there is ongoing discussion regarding the reclassification of prescription medicines to over-the-counter (switch OTC) status, and we expect gradual progress in this area. However, the impact on our business will likely be limited to certain categories such as eye drops, dermatological products, and diagnostic kits. While we expect some contribution from these areas, we do not regard switch OTCs as a major strategic pillar for the company as a whole. Instead, we will continue to focus on developing proprietary technologies and innovative products that can generate demand independently of the switch process.

Q13. What Is the Outlook for Our Prescription Pharmaceuticals–Related Businesses?

Regarding the ophthalmic pharmaceutical operations of our subsidiary Rohto Nitten, despite the challenging environment of ongoing NHI drug price reductions, we continue to generate profits through corporate efforts such as fully utilizing our production facilities by manufacturing and selling our own products while also undertaking OEM production for other companies.

In contact lenses, although we are a later entrant with lower brand recognition, sales are gradually increasing as we continue to introduce competitive products from overseas partners. In recent years, we have also strengthened our position as a specialized manufacturer by expanding our lineup of products used in ophthalmic procedures—such as lacrimal duct tubes acquired from other companies—thus pursuing growth opportunities even at a smaller scale. Looking ahead, we expect the prescription ophthalmic market to expand overseas, and we plan to leverage Rohto Nitten’s technologies and know-how to capture this growth.

Q14. We Intend to Strengthen R&D—In Which Fields Do We Compete, and What Are Our Advantages?

In our existing domains of eye care and skin care (including hair care), our basic research and product development teams have worked closely to commercialize products swiftly. Going forward, we will further advance fundamental, cell-level research. To that end, building robust collaborations with academia is essential. In eye care, we have supported young researchers for 25 years through the Rohto Award, and many awardees now serve as leading figures in Japan’s ophthalmic research. Through this initiative, we have built connections with top experts across multiple fields, forming a strong foundation for future R&D. Similarly, our networks cultivated via the Geriatric Dermatology Research Fund and the Japanese Dermatological Association’s Dermatological Research Fund have grown, and we are recognized as a distinctive presence among pharmaceutical companies.

On the intellectual property front, in the “Pharmaceutical Industry Patent Asset Scale Ranking 2024,” we ranked sixth, alongside 1) ROCHE, 2) MERCK, and 3) PFIZER, demonstrating strong deterrent power to other pharmaceutical companies. In this way, our R&D capabilities—though not fully visible on financial statements—constitute a highly powerful competitive resource.

On the other hand, in terms of intellectual property such as patents acquired through collaborative research, Rohto is ranked 6th in the "Pharmaceutical Industry Patent Asset Size Ranking 2024," alongside ROCHE in 1st place, MERCK in 2nd place, and PFIZER in 3rd place, demonstrating its strong ability to restrain other pharmaceutical companies. In this way, R&D capabilities are a competitive advantage that cannot be read on financial statements, but in reality they are a very powerful competitive resource.

Well-being Report 2025 (P49-50)

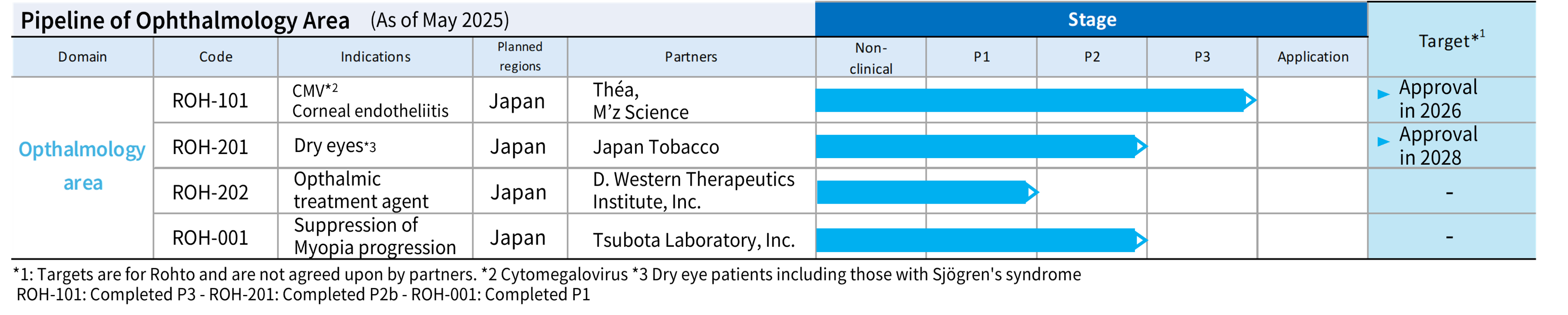

Q15. What Is the Outlook for New Ophthalmic Drug Development? What Are the Expected Scale and Profitability?

Our development pipelines are generally progressing as planned, with some candidates approaching the stage of regulatory submission. While, for strategic reasons, we do not disclose details on additional assets or the projected scale of each business, we are targeting clear unmet medical needs and areas with substantial global market potential, and we therefore expect to secure sufficient profitability over the long term.

New drug development inherently carries the risk that anticipated efficacy and safety may not be confirmed in clinical trials. However, many ophthalmic eye drops candidates are developed after mechanisms of action have already been validated in oral or other systemic therapies, and relevant data on efficacy and safety are relatively well accumulated—reducing development risk compared with other modalities. With respect to the significant clinical trial costs, we will continue to evaluate overall profitability with rigor and make strategic go/no-go decisions accordingly.

Q16. What Business Opportunities Does Rohto Foresee in Medical Fields Beyond Ophthalmology?

We see opportunities in dermatology and musculoskeletal/orthopedics. In dermatology, our DRX series—clinic-exclusive cosmetics—has built a strong track record over more than 20 years. With aggressive market expansion by Korean players, we expect the category to grow further. Rather than pursuing reimbursed prescription drugs, we aim to expand professional skin care (including hair care) used under dermatologists’ supervision to drive growth in the dermatology field. We have also successfully developed the “Autologel” PRP therapy system for refractory ulcers and launched it in January 2025, marking a significant step toward improving patient quality of life. We will expand its adoption to benefit more patients. In musculoskeletal/orthopedics, we are advancing products for knee cartilage repair using cultured chondrocytes, materials for meniscus repair, and investments in ventures related to these areas. We believe maintaining healthy, active mobility is central to well-being, especially in a longevity society.

In recent years, we have also succeeded in developing a PRP therapy system (Autologel®), a treatment system for intractable ulcers, which was launched in January 2025. This marks a groundbreaking step in improving patients' quality of life, and we will continue to expand this system so that we can contribute to the treatment of intractable ulcers for even more patients.

In the field of musculoskeletal and orthopedics, we are developing products aimed at repairing knee cartilage using cultured chondrocytes, developing materials aimed at meniscus repair, and also investing in venture companies in related fields.We believe that being able to walk healthily and energetically leads to improved well-being, and is extremely important in a society where people live longer.

Q17. What Are the Approval Timeline and Business Scale Expectations for Cell-Based Products?

We are progressing multiple cell-therapy pipelines and anticipate approvals from 2030 onward. Given regulatory and pricing uncertainties in this field, we are planning conservatively for business scale. Among the targets, knee joint cell therapy is already moving toward practical adoption, and we expect steady market formation in a super-aged society. Interstem Co., Ltd., our subsidiary, is advancing a chondrocyte product designed to offer advantages over existing technologies. Post-approval commercialization may not be conducted solely by us; we will also consider out-licensing and explore international co-development/licensing opportunities.

After obtaining approval, we will not necessarily handle all sales of these products ourselves, but will explore the possibility of out-licensing them to other companies and also consider international joint development/licensing overseas.

Q18. How Much Has Rohto Invested in Regenerative Medicine, and What Are the Mid- to Long-Term Return Expectations?

Over the past 15 years, our total investments related to regenerative medicine—equity stakes and acquisitions—amount to approximately ¥10 billion. Looking ahead to 2030, within a total M&A budget of ¥50 billion, we will pursue opportunities as appropriate. On development costs, the largest component is clinical trial expenditure. To date, cumulative spend is around ¥2 billion, and going forward we expect ¥1–2 billion per year on average, subject to annual variation. Continuation decisions at each clinical stage will be made strategically, based on the then-prevailing market outlook.

Q19. In an Era of Intensifying Global Competition in Cell Therapies, How Will Rohto Compete?

Many global players from adjacent industries are entering cell therapy with growing investment scales. We remain distinctive in covering the continuum from basic research to manufacturing and clinical application. While the overall field is expected to become a sizable industry, we do not foresee dominance by a few players; rather, a diverse ecosystem of specialists will emerge. We aim to act as a connector and leader, integrating capabilities across domains to develop new treatments.

Q20. What Is the Outlook for the Contract Manufacturing/Processing of Cells? How Will Rohto Compete Against Large New Entrants?

Leveraging know-how cultivated through our own development, we differentiate by closely addressing client needs. Our strengths include cell culture technologies, media development/customization tailored to cell type and indication, and end-to-end support from development through regulatory submission. Beyond cell-therapy manufacturing, we are also moving early into new modalities such as extracellular vesicles (EVs, including exosomes). These initiatives position us to sustain growth and demonstrate unique strengths even as large cross-industry players enter the market.

Q21. Is It Too Risky for Rohto to continue Regenerative Medicine Business? Should Rohto Focus on Conventional Business Like Skin Care?

Regenerative medicine is relatively immature and regulatory frameworks are still evolving, so volatility risks are real. However, compared with new chemical entity development, cell-based approaches—leveraging intrinsic human cell functions—can offer favorable safety and multi-faceted mechanisms, with potential to address diseases previously beyond reach. Our strength lies in the cross-fertilization of cell and regenerative research with product development in eye care, skin care, and oral categories—making these technologies both essential and broadly applicable. As competition (especially global) shifts toward cell-level science, owning frontline knowledge and IP becomes a decisive advantage. Our cell-science foundation also underpins basic research for skin care and beyond—an advantage versus ventures focused solely on pharmaceuticals.

Our strength is that this basic research in Regenerative medicine and cell research can be utilized in future product development in the fields of eye care, skin care, and oral medication, and has become an essential technology. Recently, attention has been focused on the function of endoplasmic reticulum (EVs) released by cells, and we believe that when the future development race, especially with overseas companies, becomes a battle of science at the cellular level, having cutting-edge knowledge or intellectual property in this field will be a major advantage. In that sense, basic research in cell research is also basic research for skin care, etc., which is a major advantage compared to ventures that only aim to develop pharmaceuticals.

Q22. What Are Rohto’s Strategy and Priorities for Global Expansion?

We position Southeast Asia as our global growth driver, sustaining high growth in core eye care and skin care while actively developing hair care, food/supplements, and medical businesses. With Vietnam and Indonesia as hubs housing our own plants and R&D, we see substantial upside in Malaysia and the Philippines. In China, we will maintain a solid Health & Beauty base while strengthening hair care and medical initiatives and developing China-specific value propositions by integrating rapidly advancing local technologies—capturing structurally growing healthcare demand. Globally, we will build “Rohto eye drops” and “Hadalabo” as worldwide brands. In eye care, we will expand into Europe centered on Mono (Austria), acquired last year. For skin care, “Hadalabo Tokyo”—launched from Poland—has achieved hits in previously hard-to-enter markets such as the UK and Australia, and will expand further worldwide. We will also continue to explore M&A opportunities to broaden the quality and geographic reach of our Healthcare/Well-being portfolio.

In China, the largest market, we will steadily maintain our health and beauty business, strengthen new businesses in hair care and medical, and promote the development of value unique to China that incorporates rapidly improving local cutting-edge technology, thereby capturing China's healthcare demand, which will continue to grow over the long term.

Furthermore, by promoting ROHTO Eye Drops and Hada Labo globally and cultivating global brands, we will spread the value of eye care and skin care worldwide. In eye care, we will expand into previously untapped Europe, centered on the Austrian company Mono, which we acquired last year. For Hada Labo, we will launch "Hadalabo Tokyo" in Poland, targeting the Western markets, and make it a hit in the UK and Australia, where skin care has previously been difficult to enter, before expanding further worldwide.

Additionally, we will continue to explore M&A opportunities to expand our healthcare and well-being businesses qualitatively and geographically.

Q23. How Does Rohto Mitigate Risks When Operating Across Many Countries?

Operating globally entails geopolitical, governance, supply, reputational, and safety risks. We have established systems to manage these prudently. For geopolitical risk, we divide overseas subsidiaries into five regions and establish region-centric manufacturing and resources, enabling procurement and autonomous operations even if logistics are disrupted. For governance, five regional headquarters enforce management aligned with our Group philosophy, and we deploy a global head-office hotline across subsidiaries. In finance, we use flat consolidation under Japan headquarters to directly manage regional subsidiaries—strengthening global governance through multiple layers.

To address governance risks, our five regional headquarters thoroughly manage our regional subsidiaries in accordance with the Rohto Group's management philosophy, and we have introduced an internal reporting system directly controlled by our global headquarters to each subsidiary.In terms of accounting and finance, we are strengthening our global governance system in a comprehensive manner, including through flat consolidation under the direct control of our Japanese headquarters, which directly manages our regional subsidiaries.

Q24. What Qualities Does Rohto Require for Future Leaders?

Next-generation leaders must combine deep scientific literacy with sound managerial judgment—including the ability to prioritize R&D investments and evaluate returns based on scientific insight. Managing a diverse portfolio—skin care, eye care, prescription/regenerative medicine, and overseas operations—requires risk-aware strategy and strong governance. In a VUCA era, we value decisive, change-oriented leadership and the ability to foster psychological safety. We seek leaders who pair strategic and scientific acumen with humanity and trustworthiness, consistent with our founding value of “respecting people.” Recognizing that concentrating all qualities in one person is increasingly difficult, we promote a team-based leadership model, with internal development and external recruitment driven by the Nominating Committee.

To achieve this, we need leadership that combines personal charm and trustworthiness with business strategy and scientific knowledge. Since our founding, we have grown together with a diverse range of stakeholders, including employees, customers, business partners, and shareholders, centered on the value of "valuing people." To survive in this rapidly changing era, we need not only the ability to make calm decisions, but also the personal qualities to inspire people and gain the trust of the organization.

However, it is expected that it will become increasingly difficult to require specific individuals to possess these qualities in the future, and we will enter an era in which management will be carried out as a "team." Our new management structure also aims for a system in which management will be carried out as a team, and going forward, it will be the responsibility of the Nominating Committee to continue to develop such human resources both internally and externally.

Q25. Rohto Has a Company with Board of Auditors. Why Not Adopt the Company with Audit and Supervisory Committee Structure?

The key difference is that an Audit and Supervisory Committee acts only by collective resolution and individual members lack authority to conduct investigations independently. By contrast, Statutory Auditors operate on an individual basis and can act swiftly—an advantage in emergencies and for governance reinforcement. We therefore prefer the Board of Auditors model and have strengthened it by appointing three outside statutory auditors to ensure full functionality.

26. The Nominating and Compensation Committees Are Voluntary Advisory Bodies—Do They Function Effectively?

Both committees serve as advisory bodies to the Board and are composed with a majority of outside directors to ensure objectivity and fairness. Members with deep understanding of our business conduct multi-faceted discussions reflecting internal and external realities. We believe the committees are fulfilling their intended roles.

Q27. Why Not Make Outside Directors a Majority on the Board?

We currently appoint five outside directors. For final decision-making, it is critical that our Board include a diverse set of directors with deep business knowledge and leadership across domains—vital for business continuity and leadership development. While outside directors are not a majority, we ensure transparency through outside-director-led Nominating and Compensation Committees and third-party evaluations. We will continue to optimize Board composition according to external conditions and corporate stage, maintaining our balanced Board—an integration of internal and external expertise—as a competitive advantage. Our Board of Auditors has a majority of independent outside auditors to further strengthen governance.

Therefore, although currently, outside directors do not make up the majority, we have established a highly transparent governance system by introducing a nomination and compensation committee led by outside directors and third-party evaluations. Going forward, we will continue to consider optimizing the composition of the Board of Directors in accordance with the external environment and management phase, while maintaining and developing our current "balanced Board of Directors that combines internal and external knowledge" as one of our competitive advantages. Meanwhile, we are strengthening governance by adopting a structure in which independent Outside Audit & Supervisory Board Member of Auditors.

Q28. The President and Chairman Do Not Use CxO Titles. How Are Roles and Responsibilities Defined?

Both roles are pivotal and closely coordinated to drive sustainable growth and value creation. Rather than a strict CEO/COO hierarchy, we operate on equal footing, leveraging respective strengths. The Chairman takes a long-term, group-wide view—crafting vision and building external networks. The President leads line organizations, executing mid-term strategy and overseeing day-to-day operations. We maintain flexibility in role allocation to respond quickly to change; this complementary model best supports our management goals.

Q29. What Is Rohto’s Basic Policy and Stance on Shareholder Engagement?

Our policy prioritizes equality and fairness, with transparent disclosure. For retail investors, we provide information via IR seminars and online briefings. For institutions, the Vice President & CFO and IR team lead meetings and sessions on strategy and finance. Feedback is shared with management and the Board to inform value-enhancing decisions. Where information is competitively sensitive or potentially misleading in a long-term context, we may refrain from disclosure after careful judgment. We adhere to fair disclosure, making proactive, principled decisions aligned with diverse investor needs.

On the other hand, we may, after careful judgment, refrain from disclosing information that must be kept confidential from a competitive or strategic perspective, or information that may cause misunderstandings about management from a long-term perspective.Our basic stance is to always adhere to fair and honest corporate activities and to thoroughly implement fair disclosure, while proactively determining what to disclose based on diverse investor needs.

Please also see our information disclosure policy.

Q30. How Are Directors’ Compensation Determined, and Why Does Rohto Not Use Performance-Linked Stock Options?

Compensation comprises base and performance-based elements. Base pay reflects role and responsibility; performance pay includes annual performance and mid-/long-term value-creation components, with the latter emphasized to align with our long-term management focus. Because mechanisms heavily influenced by short-term earnings or share price do not fit our philosophy, we do not adopt stock options commonly used elsewhere. Our program is designed to incentivize correct long-term decision-making.

Q31. How Does Rohto Think About the Cash Position on the Balance Sheet?

Our financial policy aims to simultaneously achieve sound balance, growth investment, and enhanced shareholder returns—delivering resilient profitability amid uncertainty and sustainably increasing corporate value. We maintain a robust equity ratio, secure sufficient operating cash and growth-investment capacity, manage capital costs, and strive to keep ROE/ROA at healthy levels through balanced, efficient treasury management.

Q32. What Is the Rationale for the Convertible Bonds Issued in February 2025, and What Are the Policies for Future Financing and Share Buybacks?

To fund the EYS acquisition, we used cash at Asian subsidiaries and bank borrowings, which increased interest-bearing debt and lowered the equity ratio from the 70% range to the 60% range. Issuing zero-coupon convertible bonds enabled us to repay bridge loans and diversify funding for share repurchases and future R&D/growth investments, maintaining a healthy financial balance. Even after issuance costs, funding was effectively at negative interest rates over the long term in a rising-rate environment. We estimate ¥20 billion of additional financing over the next six years, choosing optimal methods consistent with our policy. Given current conditions, no near-term buybacks are planned; future decisions will weigh our financial balance, investment pipeline, and market valuation.

We are planning to raise 20 billion yen over six years, and will select the best method of fundraising based on our financial policy. As for share buybacks, given the current situation, we do not have any plans for them in the near future, but in the future we will make a comprehensive decision based on our financial balance, the status of investment projects, and the state of our company's valuation in the market.

Q33. What Is the Basic Stance on M&A?

Our M&A objective is to enhance customer value by partnering in new businesses, channels, or regions where we lack presence. With a solid cash position, we evaluate targets for mid-/long-term profitability and limited margin dilution. Rather than large deals like EYS, we target cumulatively ¥50 billion by 2030, selecting opportunities that fit our growth strategy and support sustainable value creation.

Q34. What Is the Rationale for Rohto’s CSV Activities? Do They Generate Returns?

Guided by our philosophy—serving society as a public entity—we place social contribution through our core business at the center of corporate activity. CSV aligns naturally with our operations, simultaneously addressing social issues and business growth. Beyond self-care and professional care, we partner with local governments, NPOs, and regional companies to tackle issues we cannot reach alone. These efforts strengthen community trust, employee engagement, and brand equity, supporting sustainable growth. While short-term, direct profit attribution is difficult, improved reputation and recognition translate into consumer support and corporate trust for our products.

In addition to the self-care and Professional care field directly linked to our core business, we also work with a variety of partners, including local governments, NPOs, and local companies, to address social issues that are difficult for us to address on our own. These activities are not just a contribution to society; they also contribute to the sustainable growth of the company by building relationships of trust with the local community, improving employee engagement, and increasing brand value.

Although it is difficult to measure returns directly as short-term revenue, we believe that improving our corporate reputation and brand recognition through support activities will lead to increased support for our products, which are supported by consumers, and foster trust in the company.

Q35. Rohto Is Expanding into Food—What Is the Probability of Success?

Our food initiatives leverage our scientific capabilities to promote healthy living. We see strong potential in supplements that can be marketed with quasi-pharmaceutical positioning, as evidenced by the success of “Rohto V5”. Diet is foundational to health and preventive care, making food integral to our social healthcare strategy. The EYS acquisition adds proven food-related business models, increasing the likelihood of success as we scale.

Q36. How Does the Performance Compare with Peers, and Is It Sustainable?

We occupy a unique position as an integrated healthcare company spanning cosmetics and OTC medicines, prescription and regenerative medicine, diagnostics, and food. While some majors compete in global brands and luxury channels, we advance science-driven differentiation—notably in skin and eye care—through product development and formulation technology. With operations in over 115 countries, we tailor brands to local needs and utilize local production, building resilience to FX and regulatory shifts. Historical results demonstrate stable, sustained growth versus peers, validating our strategy, and we have achieved 21 consecutive years of dividend increases. We aim to continue steadily enhancing shareholder value.

We have expanded globally to over 115 countries, and have built a business model that is more resilient to changes in the external environment than our competitors through flexible brand development and local production tailored to local needs. This operational flexibility is a competitive advantage in the healthcare industry, which is particularly susceptible to the effects of currency exchange rates and regulatory fluctuations.

In fact, looking at past performance trends, it is clear how stable and sustainable our growth has been compared to our competitors, demonstrating the effectiveness of our strategies. We have also increased dividends for 21 consecutive years, and we expect to continue to steadily increase shareholder value.

*The average of five companies in the same industry was selected from companies in the same industry (cosmetics, consumer goods, and pharmaceutical manufacturers) that are similar in size and business area to our company.

*The listed multipliers represent growth over the past 10 years.

Q37. What Is the ESG Stance?

In line with our Articles-based philosophy and Seven Declarations (values code), we work with all stakeholders—consumers, partners, employees, investors, and communities—to realize a well-being society and enhance corporate value. We have identified five materialities: Well-being through business, maximizing human capital, contributing to a sustainable environment, coexistence with society, and strengthening the management foundation. ESG is central to strategy, and we also emphasize “Health (H)” as a core value, promoting ESH management, which directly links to management incentives.

These are guidelines for simultaneously achieving business growth and creating social value. At the same time, the Group places ESG at the core of its management strategy. In addition to ESG, the Group also promotes "ESH Management," which places "Health (H)," a core value, as an important perspective. This is an important indicator that is directly linked to the incentives of management.

Q38. What Is Rohto’s View on DEI?

To continuously create value amid diversification and globalization, diverse talent must share values, challenge one another, and grow together. We cultivate an inclusive culture with high psychological safety, advancing diversity initiatives. Examples include long-standing support for women’s advancement (now 30%+ women managers), policies for LGBTQ+ inclusion (e.g., same-sex partner registry, SOGI conduct guidelines), increased hiring and inclusion of global talent, and inclusive disability employment practices.

Q39. What Is the ROE Target? It Is Lower Than Some Global Peers—Will You Try to Raise It?

ROE is a key measure of shareholder value creation. For FY2024, our ROE was 12.1%, sustaining double digits while in an investment phase—evidence of healthy efficiency relative to peers. Forcing ROE up to global-mega levels is neither sustainable nor effective given scale differences. Our policy is to maintain double-digit ROE and raise corporate value through steady, continuous growth.

Looking ahead, forcibly raising this level to the same level as major global companies is not considered a sustainable or effective strategy given the current overwhelming difference in corporate size and financial strength.

Therefore, we intend to continue to increase our corporate value by maintaining a double-digit ROE and growing our business in a sustainable manner.

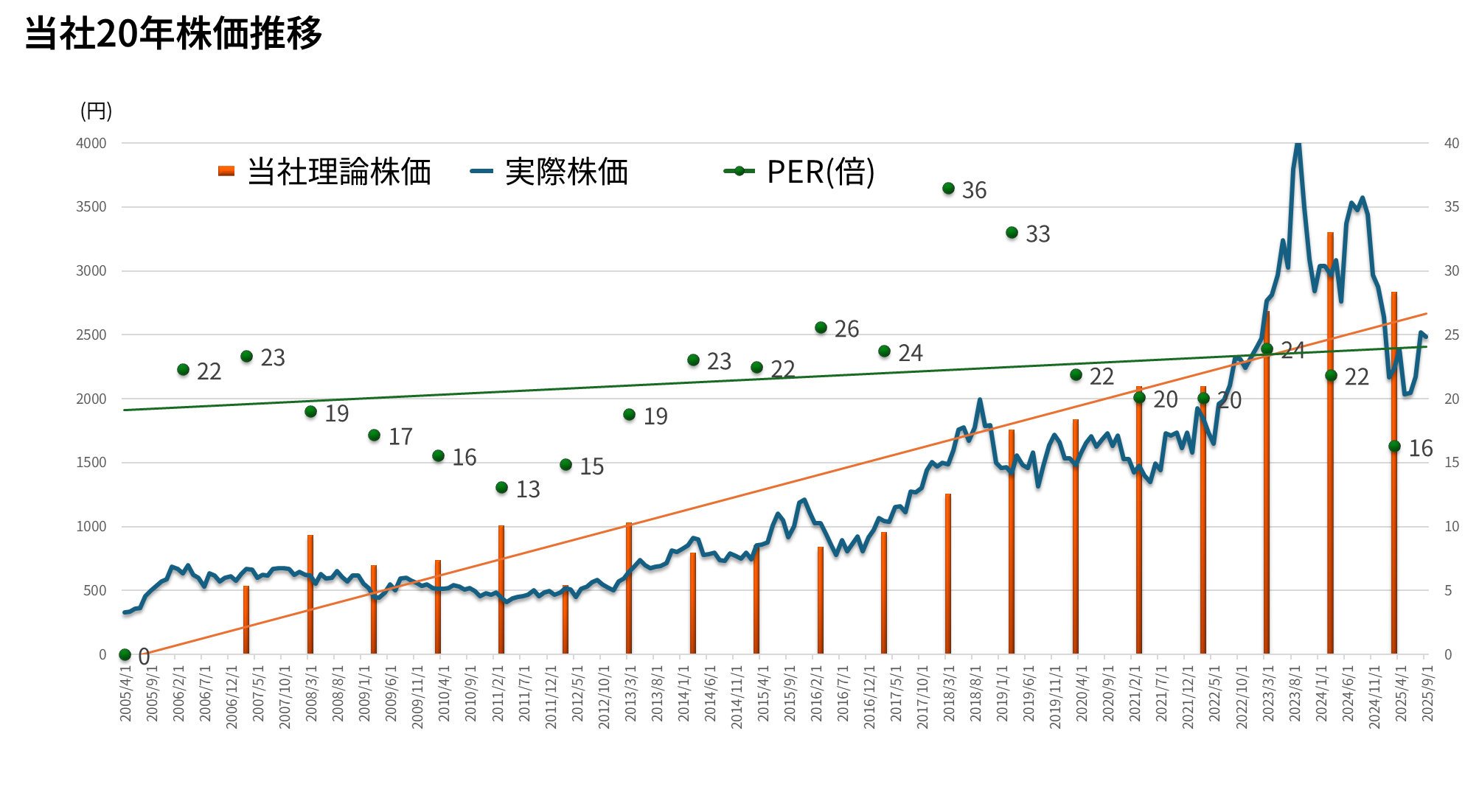

Q40. What Is Rohto’s View on the Share Price?

Share prices fluctuate with market conditions and investor behavior; by law and prudence, we do not act to directly influence daily price movements. Our focus is sustained, long-term value creation, which guides all decisions. Over the past 20 years, corporate value has steadily increased and has tracked with the share price over the long term. We commit to consistent, decisive management rooted in this philosophy for all stakeholders.

Theoretical stock price: Theoretical stock price calculated by combining the market capitalization calculated using the DCF method based on the FCF for the fiscal year in question and the market capitalization calculated using the multiple method using the EBITDA multiple for the two fiscal years immediately preceding the fiscal year in question.

The information presented on this page is as of September 2025. For details regarding our disclaimer, please refer to here for the disclaimer.